Over the past 15 years, property ownership has become increasingly accessible, empowering young investors to acquire real estate for rental income.

While it is possible to start a rental investment project at any age, it is important to establish clear objectives. It’s all about making the right decisions, and getting the right advice and support so that you can be successful in your venture, no matter your age.

In this article, OVO Network examines investment prospects for different age groups: 20-30, 30-40, and over 50, to uncover their unique benefits.

Investing in your 20s

Investment goals

If you’re in your 20s, investing in a holiday rental chalet can be an excellent way to prepare for the future and build your assets from an early age. It’s also a way of becoming financially independent, by generating additional income through seasonal rental.

What’s more, a successful investment at a young age can convince banks of your financial credibility, seriousness and commitment which will help you plan and realise future property projects.

Financing your invesment

The purchase of a chalet can be financed in a number of ways. You can cover an investment from your own funds, or take out a mortgage.

In the latter case, if you want to get the best interest rate, we recommend that you carry out a full market study and draw up detailed business plans, including various rental income generation and profitability forecasts. This will demonstrate the financial credibility of the project to the lender.

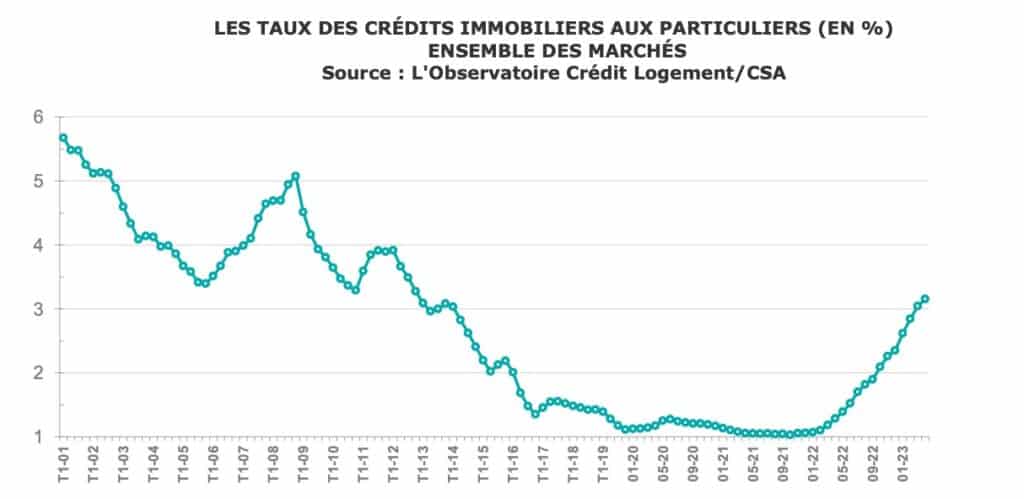

Mortgage rates have recently risen sharply. Please note: the interest rate depends on many factors relating to the project, such as the borrower’s situation, the term of the loan and the bank selected. It is therefore essential to contact different banks to obtain more precise information about the potential loan, and to negotiate the terms.

Younger borrowers can opt for long-term home loans, such as 25 or 30-year mortgages. This reduces the monthly repayments and makes the amount more affordable for borrowers on lower incomes.

In addition, banks often seek to establish a long-term relationship with their customers. By granting a home loan to a serious young investor, they have the opportunity to develop a relationship early on in the borrower’s financial life, with the prospect of providing other financial services in the future.

Investing in your 30s

Investment goals

For the 30-40 age group, rental investments serve multiple objectives, such as generating additional income, launching new ventures, or building a property portfolio, ensuring long-term financial security and diversification.

These investments often stem from a desire to benefit from tax advantages, with laws like the Pinel Law providing tax reductions for investments in new or renovated properties, and the Malraux Act applying to protected areas or zones for the protection of architectural, urban and landscape heritage (ZPPAUP) . Understanding the specific conditions of each scheme is crucial in making informed investment decisions.

Various rental statuses can aid in reducing taxes on income. For instance, the non-professional furnished rental scheme (LMNP) benefits investors who own furnished rental properties, offering tax advantages like property and furniture depreciation. This deduction lowers the taxable rental income, reducing the tax burden.

Additionally, rental-related expenses such as management fees, co-ownership charges, and insurance costs can be deducted to optimise profitability. For personalised advice on the LMNP scheme or others, consult a chartered accountant or tax adviser, as rules and conditions may differ based on individual project circumstances.

Financing your invesment

For those aged 30-40, it is also common to take out a mortgage to finance the investment. The first step is to carry out a financial capacity assessment which includes an examination of income, expenditure, savings and debts. This will provide you with a realistic idea of your investment, borrowing and repayment capacity.

If you have savings or cash available, you may be able to use this money as a downpayment. A personal deposit reduces the amount of the loan required and can improve the borrower’s profile in the eyes of the banks. If possible, make a deposit of at least 10-20% of the purchase price of the chalet. A larger deposit demonstrates the investor’s confidence and commitment to the project, which may attract more interest from the banks.

Once again, it’s vital to seek professional advice. Their specific advice can help you make the best choices to optimise your investment.

Investing at 50+

Reasons for investment

For the over-50s, the reasons for investing in rental property are often different. Firstly, it can be a way of anticipating retirement by securing regular additional income – in other words, it can contribute to financial security. Secondly, it can be an attractive way of taking early retirement, achieving a degree of financial independence, or even keeping working during retirement, for those who don’t want to stop working altogether.

Owning a rental chalet also allows you to build up an estate that you can pass on to your heirs. It is possible to benefit from the property’s appreciation over time, which can increase its net value and offer significant opportunities for capital gains on resale.

Financing your investment

When it comes to financing your investment, you have two primary options: using your savings or taking out a loan. If you already have outstanding loans, consolidating them into a single loan is a viable choice. This consolidation simplifies repayment management and may lead to reduced monthly payments.

At any age, it’s still important to consider certain aspects when investing in a holiday rental chalet. For example, you need to take into account the geographical location, tourist demand, maintenance and management costs, and local regulations on holiday lets. Knowing this information will enable you to correctly anticipate the profitability of the project.

Generally speaking, investing in a holiday rental chalet is accessible to all ages. Whether you want to prepare for the future, earn extra income, save on tax, build your assets or secure your retirement, investing in a holiday rental chalet can offer many advantages.

What’s more, there are various financing options available to future investors, depending on their abilities and needs.

However, it’s essential to surround yourself with professionals when taking the necessary steps. Our team of advisers at OVO Network are here to help future homeowners with their plans. They can help them determine the best investment and financing strategy for their specific needs and objectives.

Here are some of our other articles on rental investment projects: